With the U.S. Federal Reserve making its first rate hike in almost a decade, investors trying to solve the low yield, rising interest rate challenge will look to products that can generate income and preserve capital in a rising-rate environment. Real estate investments may help navigate this headwind.

History illustrates that commercial property returns have more often increased than decreased during periods of rising interest rates. As discussed herein, real estate shows a pattern of positive returns during many times of rising interest rates over the past 20 years.

It may very well be the same this time around. Concern over rising rates is typically a temporary occurrence because, by the time a rate movement has begun, impacted sectors tend to have already discounted the action.

If interest rates rise due to an improving economy, commercial real estate values are likely to strengthen as a result of higher rents, higher occupancy and better overall business fundamentals. Economic growth also fuels corporate spending, consumer spending and employment.

Owners of commercial real estate also have the capacity to raise rents. In asset classes with shorter-term leases, such as multifamily and some smaller retail spaces, leases roll on a more frequent basis. Therefore, landlords have more power to raise rents to keep pace with rising interest rates.

A Spring in its Step

Commercial real estate returns have shown a pattern of resilience. The current economic environment is similar to the 2004-2006 period, when the Fed gradually began raising rates after a long period where rates had been rather low. The initial drop in real estate returns is shown during the first quarter of 2004 and is followed by consecutive periods of increasing returns. If the goal is income, reviewing the history of real estate returns during periods of rising interest rates suggests opportunity for income potential.

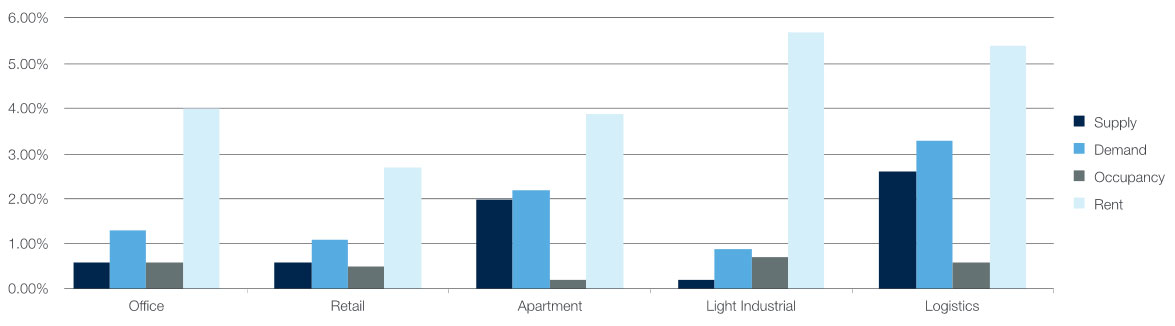

Key Statistics For Major U.S. Property Sectors

Year-Over-Year Change as of Q2 2015

Source: CoStar. Construction Not Keeping Up with Demand In Light Industrial Market. August 12, 2015.

NCREIF Property Index Returns

Highlighted Areas are Times of Rising Interest Rates

| Quarter 1 | Quarter 2 | Quarter 3 | Quarter 4 | |

|---|---|---|---|---|

| 1996 | 2.40% | 2.29% | 2.63% | 2.61% |

| 1997 | 2.34% | 2.82% | 3.38% | 4.71% |

| 1998 | 4.14% | 4.19% | 3.46% | 3.55% |

| 1999 | 2.59% | 2.62% | 2.81% | 2.89% |

| 2000 | 2.40% | 3.05% | 2.94% | 3.33% |

| 2001 | 2.36% | 2.47% | 1.60% | 0.67% |

| 2002 | 1.51% | 1.61% | 1.79% | 1.67% |

| 2003 | 1.88% | 2.09% | 1.97% | 2.76% |

| 2004 | 2.56% | 3.13% | 3.42% | 4.66% |

| 2005 | 3.51% | 5.34% | 4.44% | 5.43% |

| 2006 | 3.62% | 4.01% | 3.51% | 4.51% |

| 2007 | 3.62% | 4.59% | 3.56% | 3.21% |

| 2008 | 1.60% | 0.56% | -0.17% | -8.29% |

| 2009 | -7.33% | -5.20% | -3.32% | -2.11% |

| 2010 | 0.76% | 3.31% | 3.86% | 4.62% |

| 2011 | 3.36% | 3.94% | 3.30% | 2.96% |

| 2012 | 2.59% | 2.68% | 2.59% | 2.53% |

| 2013 | 2.57% | 2.87% | 2.59% | 2.53% |

| 2014 | 2.74% | 2.91% | 2.63% | 3.04% |

| 2015 | 3.57% | 3.14% | 3.09% |

Source: NCREIF. The National Council of Real Estate Investment Fiduciaries (NCREIF) Property Index (NPI) is an index of quarterly returns reported by institutional investors on investment grade commercial properties owned by those investors. The NPI is used as an industry benchmark to compare an investor’s own returns against the industry average. The NCREIF Property Index is an index of quarterly returns on an unleveraged basis reported by institutional investors on investment grade commercial properties owned by those investors. While not a measure of nonlisted REIT performance, Inland Real Estate Investment Corporation generally believes that the NCREIF Property Index is an appropriate and accepted index for the purpose of evaluating real estate growth rates. The NCREIF Property Index does not reflect management fees and other investment- entity fees and expenses, which lower returns. Indices are not available for direct investment. The NCREIF Property Index is based on appraisals and does not reflect the same market volatility as the NAREIT Equity Index, which is based on market prices of publicly-traded REIT securities. Index performance may differ significantly from a REIT. Additionally, a REIT has fees and expenses not found in an index. Past performance does not guarantee future returns.

Over the past 20 years, 42 quarters have been affected by rising interest rates, with commercial property returns being positive 39 of those quarters.

As the Fed continues to taper its quantitative easing program, real estate investors may experience fluctuating returns in the short- term. That being said, as long as strong underlying real estate fundamentals persist and the U.S. economy continues to grow, the outlook for real estate investments likely remains positive.1

Hedge Against Inflation

Since most scenarios of rising interest rates triggers conversations of inflation, an added benefit of real estate investments is their ability to generally provide natural protection against inflation because of higher rents and values.

The income from commercial real estate is driven by supply and demand. With new construction at historical lows, demand is high while supply is limited, which leads to higher rental rates. Values and prices tend to increase when rental rates do, supporting growth in net operating income and providing a reliable stream of income even during inflationary periods.

While rising interest rates should warrant a review of real estate investments, there is an upbeat outlook for commercial property performance. Since gradual rate increases and inflation would be products of a stronger economy, the focus can return to the strong fundamentals underlying commercial real estate values.

Sources:

1REIT.com. Misconceptions About REITs and Interest Rates. May 18, 2015.

Disclosure

The views expressed herein are subject to change based upon economic, real estate and other market conditions. These views should not be relied upon for investment advice. Any forward-looking statements are based on information currently available to us and are subject to a number of known and unknown risks, uncertainties and factors which may cause actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by these forward-looking statements.

Important Risk Factors to Consider

Some of the risks related to investing in commercial real estate include, but are not limited to: market risks such as local property supply and demand conditions; tenants’ inability to pay rent; tenant turnover; inflation and other increases in operating costs; adverse changes in laws and regulations; relative illiquidity of real estate investments; changing market demographics; acts of God such as earthquakes, floods or other uninsured losses; interest rate fluctuations; and availability of financing. Some of the risks specifically related to investing in a non-traded real estate investment trust (or “REIT”) include, but are not limited to:

- The board of directors, rather than the trading market, determines the offering price of shares; there is limited liquidity because shares are not bought and sold on an exchange; repurchase programs may be modified or terminated; a typical time horizon for an exit strategy may be longer than five years; and there is no guarantee that a liquidity event will occur.

- Distributions cannot be guaranteed and may be paid from sources other than cash flow from operations, including borrowings and net offering proceeds. Payments of distributions from sources other than cash flow from operations may reduce the amount of capital a REIT ultimately invests in real estate assets and a stockholder’s overall return may be reduced.

- Failure to qualify as a REIT and thus being required to pay federal, state and local taxes, which may reduce the amount of cash available for distributions.

- Principal and interest payments on borrowings will reduce the funds available for other purposes, including distributions to stockholders. In addition, rates on loans can adjust to higher levels, and there is a potential for default on loans.

- Conflicts of interest with, and payments of significant fees to, a business manager, real estate manager or other affiliates.

- Tax implications are different for each stockholder. Stockholders should consult a tax advisor.

Publication Date: 5.20.16